In H1, SHFE copper experienced rollercoaster fluctuations, with its price movements closely tied to US tariff policies, albeit driven by divergent logics. The Q1 copper price rally stemmed from expectations that the US might impose additional tariffs on imported copper. Fears of rising import costs propelled COMEX copper's sharp gains, lifting LME copper and SHFE copper, with the latter peaking at 83,000 yuan, hitting a one-year high. However, the uptrend proved short-lived. As the US unexpectedly implemented reciprocal tariffs and other nations escalated countermeasures, market concerns intensified over potential global supply chain disruptions that could stifle growth and fuel inflation. Copper prices plunged from highs, entering a prolonged recovery phase before SHFE copper eventually reclaimed the 80,000 yuan threshold.

Phase 1: Early January to late March

Macro front, initial US tariff hikes were relatively small, coupled with softening US economic data and temporarily dovish US Fed policy expectations. The US dollar index slumped to a five-month low, buoying copper prices. Supply and demand side, spot TC for domestic copper concentrates kept declining, with persistent worries about ore tightness transmitting to smelting sectors. Additionally, the US earlier announced plans for 25% tariff hikes on steel and aluminum products, sparking market anticipation of potential copper tariffs. This prospect of higher US copper import costs and inflationary pressures made COMEX copper outperform LME and SHFE copper, though initial tariff rate expectations hovered around 10%-15%. Subsequent US Section 232 investigations on copper, with officials hinting at possible 25% tariffs—significantly above prior estimates—further elevated future import cost projections. COMEX copper's price center kept rising, propelling SHFE copper above 80,000 yuan.

Phase 2: Late March to early April

Early April saw unexpected US reciprocal tariffs and intensified foreign countermeasures, amplifying market fears that fractured global trade chains could hamper growth and accelerate inflation. Risk assets faced broad selloffs, with base metals plunging to cycle lows. SHFE copper erased all year-to-date gains, bottoming at 71,320 yuan—an eight-month low.

Phase 3: Mid-April to June-end

The US initiated negotiations with multiple countries. After China-US reciprocal tariffs were temporarily cut to 10% for 90 days, markets briefly priced in tariff de-escalation. However, slow progress in some talks and Trump's unpredictable stance kept concerns alive about renewed trade friction post-grace period. As optimism faded quickly, macro uncertainties resurfaced, leaving copper prices to grind higher in rangebound fluctuations. At month-end in June, US Fed officials delivered dovish testimony in Congress, raising expectations for interest rate cuts. The US dollar index continued to weaken, hitting new lows, and copper prices began to rally. However, it was the off-season for traditional metal demand. Although most varieties did not see significant inventory accumulation, the weak demand limited the upside potential.

US Reciprocal Tariffs Cause a Stir, Uncertainty Intensifies Amid De-globalization

Due to the large scale of US debt and severe trade deficits, the new US president has been wielding the tariff stick since taking office to divert domestic conflicts. Although in retrospect, the policies seem to have been raised high but implemented lightly, the increase in trade barriers and the escalation of geopolitical frictions have intensified regional fragmentation and uncertainty. Looking back at the changes in tariff policies in H1, on April 2, the US implemented unexpected reciprocal tariffs, followed by other countries' escalating retaliatory measures, which led to a sharp rise in market panic and a widespread sell-off of risky assets. However, as the US dollar liquidity crisis worsened, concerns over debt and economic growth rose, and the US trade attitude towards other countries warmed, with negotiations starting one after another. Currently, it is the buffer period for reciprocal tariffs. Recently, there has been good news from Sino-US economic and trade negotiations, with the US side set to cancel a series of restrictive measures against China accordingly. However, the negotiation window between the US and Europe is normally set to end in the first half of this month, and Trump's attitude is relatively unpredictable. Although the market has become somewhat desensitized to this, if reciprocal tariffs are indeed implemented, it could still dampen market sentiment. Therefore, it is still necessary to track changes in the US government's external tariff policies.

Smelters Persistently Maintain Production, Long-term Contract Processing Fees "Zero Out"

In recent years, the tightness of ore supply and extremely low processing fees have become major contradictions in the copper market that cannot be ignored. Moreover, as of today, these contradictions have not eased but rather intensified. Looking back at the decline in processing fees, it started with the closure of the Cobre Panama copper mine in Panama at the end of 2023. Previously, the mine had an annual output of 350,000 mt, accounting for 1.5% of global supply. Although the proportion was relatively small, the mine mainly supplied to China, so the loss of this copper ore supply dealt a blow to domestic spot processing fees, which showed a trend of falling back from highs. However, countries like Chile and Peru are the main suppliers of copper concentrates to China. Normally, there would be other sources of copper ore to supplement the supply, and the loss of a single copper mine supply obviously could not cause processing fees to fall to such extremely low levels. Nevertheless, observing the performance of domestic copper concentrate spot processing fees in recent years, it can be seen that after rapidly declining to single-digit levels, processing fees stabilized in H2 of 2024, only to break down again this year, falling to negative values and still struggling to rebound. Currently, they hover around -$40/dmt. Such extreme processing fees are astonishing, and the reason lies in the fact that the expansion speed of smelters has been faster than that of copper mines, leading to a continuous tight supply and demand situation for copper mines and an increasing bargaining power for mines.

Copper concentrate treatment charges (TCs) are crucial to the production profits of smelters. A negative TC obviously increases the production pressure on smelters. Generally, domestic smelters concentrate their maintenance periods in Q2. However, in March this year, Tongling Nonferrous Metals Group announced maintenance news, indicating an earlier maintenance schedule that reflects the intensifying difficulties faced by smelters. Nevertheless, with most smelters having signed long-term contracts and actively promoting adjustments to their raw material structures, the substitution of copper scrap and copper anode for copper concentrates has increased. Coupled with the revenue from by-products such as sulphuric acid, gold, and silver, normal production is still being maintained, and domestic copper cathode production remains high. However, at the end of last month, the results of the mid-year negotiations between Antofagasta and Chinese smelters for 2025 were announced. The long-term copper concentrate TCs (TC/RC) for 2026 were finally locked in at $0/dmt and 0¢/lb, a significant drop from $21.25/dmt and 2.125¢/lb in 2025, setting a new historical low. For smelters, zero TCs mean direct production losses. Whether the revenue from other by-products can fully cover production costs remains questionable. It is expected that the production pressure on smelters will become increasingly severe in H2. However, before a decline in the operating rate of smelters occurs, the tightness of ore supply can only provide a certain level of downward support for copper prices and is unlikely to bring more upward momentum. Subsequent tracking of smelter operations and changes in copper cathode production is still necessary.

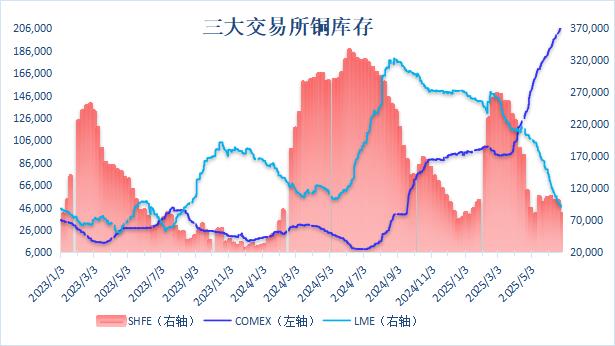

Tariff Expectations Trigger Siphon Effect, Global Copper Cross-Regional Flows

The logical drivers brought about by the US imposing tariffs on bulk commodities are slightly different from the normal logic of a trade war. In a trade war, the market is more concerned about the rise in trade barriers suppressing industrial product demand. Although it may push up inflation, the driving force is more inclined to be bearish. However, the expectation of imposing tariffs on copper and other commodities tends to drive short-term movements in related commodity prices. The main reason is that the market worries that if copper becomes a target for taxation, it will directly increase the import cost of US copper, thereby pushing up US copper prices. Due to the existence of arbitrage opportunities, the rise in overseas markets will inevitably transmit to the domestic market. Given the relative strength of US copper, the price spread between COMEX copper and LME copper has remained near historical highs this year, with the current premium still above $1,000. Under the background of such a high price spread, driven by interests, global copper is flowing into the US. From the perspective of visible inventory changes, COMEX copper inventories have continuously climbed from less than 100,000 mt at the beginning of the year to over 220,000 mt now, with an increase of more than 100%. LME copper inventories, on the other hand, have continuously declined from around 270,000 mt at the beginning of the year to around 95,000 mt now, with a considerable decrease. In addition, Q2 is traditionally the off-season for domestic demand. However, influenced by the US siphon effect, the export window has remained open continuously. Smelters have successively arranged for the export of copper cathode, making it difficult for domestic inventories to accumulate significantly during the off-season. Currently, inventories are only maintained at around 130,000 mt, far below the level of the same period last year.

Since the US initiated a Section 232 investigation into copper, the timing of specific tariff measures has been a hot topic of discussion in the market, with constant rumors. Recently, a US official stated that the US is currently focusing on reciprocal tariffs and will leave the issue of industry tariffs for later, which may imply that it will take some time for the US copper tariff policy to be implemented, and traders will still have the momentum to ship copper to the US. However, recently, there has been a stabilization and rebound in LME copper inventories. Although the current rebound is limited, it can be seen that registered warrants bottomed out and rebounded in early June. In the short term, the space for destocking LME copper inventories may be relatively small. In addition, it is worth noting that before the policy is implemented, the market is still in the stage of buying expectations. However, once the policy is implemented, there is a possibility of a pullback in US copper prices. If the tariff rate is lower than previous expectations, the pullback may be even greater.

Looking ahead to the future performance of the copper market, the following key themes will be the focus of tracking: On the one hand, there is no doubt that this year will still be a significant year for macro factors. Changes in the US's external tariff policies will continue to affect demand expectations and sentiment, and vigilance is needed against the impact of black swan events on the market. On the other hand, the copper ore supply tightness situation is becoming increasingly severe, adding to the difficulties faced by smelters in their production and operations. However, it is still uncertain whether and when specific production cuts will occur. If the reduction in smelting capacity can indeed materialize, it will undoubtedly provide strong support for copper prices. Finally, the timing of the implementation of the US's copper-related tariff policies and the tariff rates imposed are also the focus of market attention. Before the policy is implemented, there will still be a window period for global copper to flow into the US. Against the backdrop of difficult-to-accumulate inventories in non-US regions, the downward momentum for copper prices is also not strong. Overall, the supply and demand dynamics of the copper market are relatively robust. However, there is significant uncertainty regarding the US's tariff policies towards other countries and its tariff policies on copper itself. It is necessary to monitor the situation as it unfolds.